The age-old question of when to retire is one that must always be asked but will never find a definitive answer.

Retire too early and you’ll run out of money in a decade.

Too late and you’ll be too old to enjoy the wealth you spent all that time building.

Everyone is different and the “ideal time” to retire will depend on countless factors.

In this article, I’m going to help you pinpoint your retirement timeline and throw in a few tips on how to retire sooner (if that’s what you actually want).

Table of Contents

How Much Do You Need to Retire?

The 4% Rule

You’ve likely heard about the 4% rule in countless articles and YouTube videos so I’ll keep this explanation quick. In a nutshell, it says that you can withdraw 4% of your portfolio every year without ever depleting the “nest egg.”

This shouldn’t be too surprising since the historical average annual return of the S&P 500 is 8.5% even after you adjust for inflation. By putting your money into ETFs like VOO or VTI, the average annual return should be more than enough to cover the amount you withdraw every year.

The question then becomes how much you need that 4% withdrawal to amount to in dollars to retire comfortably — and have enough spending money to do the things you want. Well, the median earnings for workers in the US was $41,535 in 2020.

To replace that income without withdrawing more than 4% of your portfolio annually, you would need a total nest egg value of $1,050,000. That may seem like a lot, especially if you’re young, but it’s more achievable than you might think.

How? The power of compound interest.

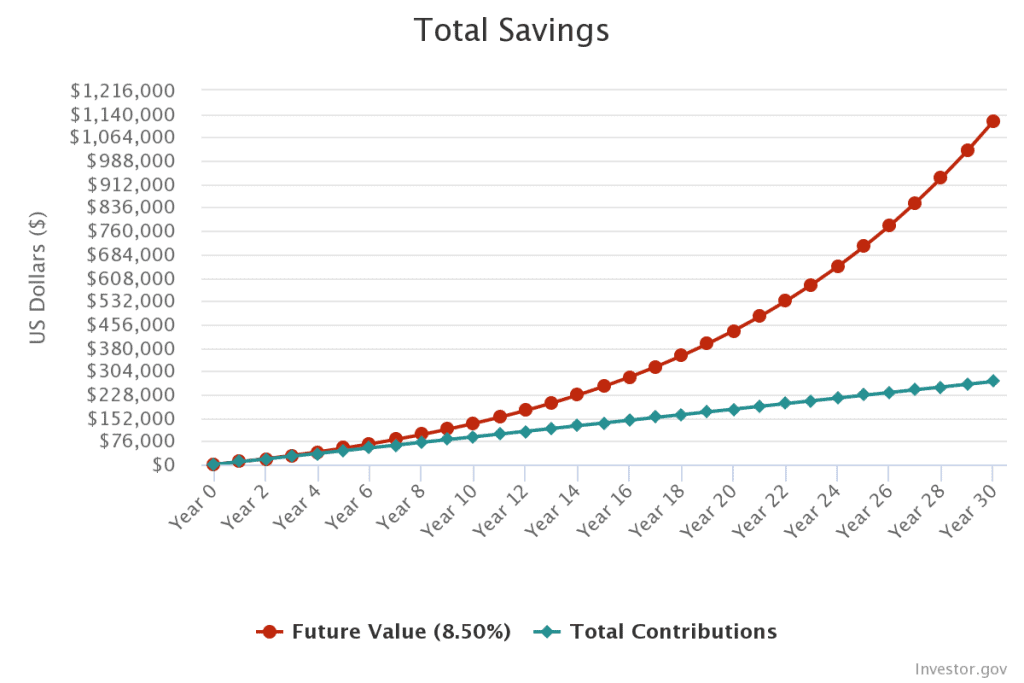

Compound Interest

Investing just $750 per month would put your portfolio at $1,117,932 within 30 years.

If you continue investing $750 per month for an extra decade after retiring then your portfolio will jump to $2,661,142. The golden rule of compound interest is starting early — and having the patience to see growth go parabolic at the end of the journey.

How to Retire Sooner

Earn More

While sticking to a strict budget and avoiding non-essential expenditure like the plague is certainly an effective (if unreasonable) strategy, there’s no denying the impact that earning more can have on your retirement timeline.

If we go back to our compound interest calculations, increasing your monthly investment to $2,000 per month would net you $1,161,048 in 20 years instead of 30. Let’s be clear, no one can snap their fingers and magically double their income.

But if earning enough to invest more can help you retire a decade sooner then isn’t it worth a shot?

Whether this comes down to getting a higher salary, building new income streams, or starting a business is up to you. The bottom line is that you have to at least consider the possibility of earning more to retire sooner rather than succumbing to self-limiting beliefs.

A few quick tips that could help you earn more include:

- Creating additional income streams

- Switching jobs every 3-4 years to maximize your salary

- Building and combining skills that make you uniquely valuable to companies

Read my full article on “How to Get a Higher Salary” for a more in-depth explanation of the principles that can turn you into a high-income individual; a title that’s both a gift and a curse, I assure you.

Spend Less

It may sound obvious, condescending even, to say that earning more and spending less are the two secrets to retiring sooner. But that’s just the thing, financial freedom is the perfect example of the difference between simple and easy.

There’s no secret to getting rich because it was never a secret in the first place. The majority of people know how they can get rich, they just never do it. In other words, it’s poor execution that keeps people, well, poor — not lack of information.

The thing is, most people think that spending less means passing on every vacation, meticulously tracking every expense, and not living out a single day of their life before they retire.

Not only is this approach unhealthy but it’s also suboptimal if you want to reduce your spending long-term. In reality, spending less really comes down to three key aspects:

- Where you live

- What you drive

- What you eat

These three Ws of expenditure, as I like to call them, have a bigger impact on your retirement trajectory than vacations or gadgets ever will. The first, and most significant, is where you live — both from a municipal and national perspective.

Whether you rent your place or get a mortgage, living in California will always be more expensive than living in West Virginia. Getting a smaller place in a cheaper city may feel like a big sacrifice but it can help you retire years, if not decades, sooner.

But why stop at moving to a cheaper city?

Emigration certainly isn’t for everyone — especially if your employer doesn’t offer remote options and/or you have family in your country of origin — but it’s worth pointing out as changing citizenship can work wonders on the percentage of income that taxes eat up.

For example, becoming a Romanian citizen means you’ll only have to pay a flat 10% income tax. With some Americans paying income taxes as high as 37%, emigrating to another country and renouncing US citizenship could free up a lot more income to invest towards retirement.

Read more — Retirement in Romania: Is Southeast Europe a Paradise?

Next up is what you drive.

Even if you buy your brand new sports car in cash, you’ll still have to insure it, pay for maintenance, and shell out money whenever an expensive part needs to be replaced or repaired.

Furthermore, brand new cars tend to lose 60% of their value in the first five years — which means you’re actively reducing your net worth from the moment you buy it. Sports cars also have higher rates of injuries compared to SUVs which could tack on additional costs in the form of medical bills and civil claims.

In summary, buying used cars (that have already depreciated in value) or opting for public transportation — like busses and trains — will reduce your spending both in the short and long terms.

Finally, look at what (and where) you eat to see if there’s an opportunity to save money without negatively impacting your health. Let me be clear, I’m not suggesting you resort to a diet of ramen and canned beans for the sake of retiring sooner.

Depriving yourself of nutrients will only cost you more when the malnutrition leads to frequent hospital visits and decreased work performance. Instead, find cost-effective and healthy ways to keep your body nourished without breaking the bank.

Buying food at the local farmers market instead of grocery stores and taking the time to cook a meal instead of ordering from Uber Eats or eating out will save you thousands every year. Don’t believe me?

The Motley Fool reported that the average US household spends $2,375 on dining and takeout every year. Homecooked meals also promote a healthier diet which leads to lower medical expenses over the next few decades.

6 Reasons You Shouldn’t Retire (Yet)

While retiring as soon as possible may seem like the most attractive or even pragmatic choice, there are quite a few reasons that say otherwise. Here are six reasons why you may want to consider putting retirement off a bit longer:

#1 Health

First and foremost, retiring too soon could be detrimental to your long-term mental and physical health. A 2016 study from Oregon State University found that working past the age of 65 could actually lead to a longer life.

Out of 2,956 participants, those who retired at 66 instead of 65 had mortality rates that were 11% lower. Correlation doesn’t always equal causation but an 18-year study encompassing thousands of people should at least get you thinking about the impact retirement will have on your health.

The most likely culprit is the sedentary lifestyle that most retirees fall into after they put their careers behind them. Regardless of when you end up retiring, throwing in regular exercise can counter the negative effects — both mental and physical — that seemingly chase those who leave the workforce.

#2 Marriage

While spending more time with your significant other seems like a great reason to retire early, there is such a thing as too much time together. Staying at home with your SO 24/7 after you retire could start to cause issues.

Even if you don’t start arguing more often than you usually do, a lack of fulfilment could develop in one or both spouses. This, in turn, may lead to feelings of anxiety or depression and a fading sense of individual autonomy.

If you’re retiring solely for the reason of being with your partner more often, make sure to balance things out by engaging in outdoor activities together and/or pursuing your own respective habits rather than turning into codependent homebodies.

#3 Fulfilment

Premature retirement can compromise the sense of fulfilment and meaning in your life. Don’t get me wrong, tying your identity and self-worth to a career path is just as damaging but that doesn’t change the fact that an early exodus from the workforce may leave you feeling empty.

This is especially true if you’ve spent most of your teens and 20s pursuing success or financial security. Tunnel-visioning on getting promoted, earning more, or hitting savings goals can leave you aimless once you reach the proverbial finish line.

It may seem cliché but Brandon Sanderson’s immortal words — “Life before death. Strength before weakness. Journey before destination.” — ring true when it comes to setting your exit timeline.

Seeing work as a means to an end will set you up for a quarter-life crisis once you retire early and there are no more goals to chase.

Trust me, I was terrified at the moment I landed my first high-paying job. Then again when I achieved financial freedom. Then even more so the moment I realized I could retire.

The remedy, of course, is to enjoy the process of working and find fulfilment in your career outside of vanity metrics like getting promoted or earning more money than you made last year.

Don’t hesitate to keep working beyond the point where you have enough money to retire comfortably. If spending time with your coworkers or making a positive impact on other people’s lives is a meaningful part of your existence, there’s no reason to cut it short.

Especially not in the name of “pragmatism,” because humans aren’t fully rational creatures.

To quote Morgan Housel, author of The Psychology of Money:

“Do not aim to be coldly rational when making financial decisions. Aim to just be pretty reasonable. Reasonable is more realistic and you have a better chance of sticking with it for the long run, which is what matters most when managing money.”

TL;DR: focus on making your career more enjoyable and fulfilling instead of trying to end it as soon as possible.

#4 Lifestyle

Working for an additional 20-30 years just so you can drive a Ferrari and live in a Manhattan penthouse is unlikely to be a worthy trade-off for most people. Still, that doesn’t mean you should treat post-retirement lifestyle as a non-factor when setting your timeline.

If you love traveling and living in the city center, staying in your job a few years longer may well be the best way to ensure you’ll be able to do the things you want after retiring. There’s no reason to rush into retirement only to fall into a lifestyle of penny-pinching when you get there.

Yes, avoiding the terrors of lifestyle inflation and overspending is a key part to setting up a secured retirement but you shouldn’t go so far as to settle for a lifestyle you’re not happy with — even if it’s in the name of retiring sooner than your colleagues.

#5 Taxes

You might think that retiring will mark the end of your tax woes since you won’t have a salary to be taxed on. Unfortunately, you’ll still have to deal with capital gains tax whenever you sell shares of index funds when cashing out of your portfolio.

Delaying your retirement will give your investments more time to grow through compound interest before capital gains taxes take a bite out of the principal. After all, you’re likely familiar with this famous quote by now:

“Our new Constitution is now established, everything seems to promise it will be durable; but, in this world, nothing is certain except death and taxes.” -Benjamin Franklin

#6 Compound Interest

Bringing this article full circle, compound interest is the last (but certainly not least) reason that may make you think twice before retiring.

Certainly, don’t trade time you don’t have for money you don’t need.

All I ask is that you find a balance between cashing out too early and waiting too long — a Goldilocks zone of when to interrupt compound interest, if you will.

To put this into numbers, let’s consider a hypothetical scenario where you put $50,000 into the S&P 500 at age 20 then let it sit with an 8.5% annual growth rate:

- By age 30 you would have $113,000

- By age 50 you would have $578,000

- By age 60 you would have $1,307,000

- By age 70 you would have $2,954,000

- By age 80 (close to the average life expectancy in the US) you would have $6,680,000

Look no further than the parabolic growth of Warren Buffet’s net worth (who made 95% of his wealth after the age of 65) to visualize the effect time has on money. In our fictional example, retiring at age 60 instead of age 30 leaves you with $1,307,000 instead of $113,000.

In the real world, the disparity between how much you’ll get to retire with becomes even larger since most savvy investors don’t just shove a $50,000 lump sum into their portfolio then never contribute to it again.

“The first rule of compounding is to never interrupt it unnecessarily.” -Charlie Munger

Finding Balance in Semi-Retirement

Once you get to the point where your annual 4% withdrawal can cover fixed expenses like housing, groceries, and gas a new option becomes available: semi-retirement.

For those who want more free time at an early age but aren’t comfortable ending their financial journey with a state of perpetual frugality, semi-retirement offers the perfect middle ground between enjoying life while growing your wealth.

With your nest egg covering all base living expenses, getting a part-time or even freelance job creates a situation where you have disposable income to spend as you please. That money could go towards a plane ticket to Malta, donating to charity, or buying that Rolex you’ve always wanted.

The best part? It’s guilt-free spending since your financial security is already secured.

As an added bonus, continuing to work — albeit during fewer hours per week — will also keep you busy, provide a lasting sense of fulfilment, and stave off the post-retirement health risks I mentioned earlier.

If you take one thing away from this article, it’s that you don’t have to wait for retirement before you start truly living your life. Transitioning to a part-time job gives you enough time to explore, enjoy, and do the things you couldn’t when you were in the rat race.

Travel the world, volunteer for non-profits, go to the gym more often, read a new book every week, pursue fun hobbies, and spend time with the people you love. Spending your time intentionally and creating unforgettable memories are things you can start doing right now.

Conclusion

As you can see, how and when to retire is a topic that’s full of nuance. No two people are alike which means there’ll never be a one-size-fits-all answer to the question. All I hope is that, by presenting you with information, you’ll be able to find a timeline that works for you.

If this article was insightful, helpful, or even entertaining then why not share it with a few friends on your social media feeds? Remember, every link you share with someone else is another opportunity for my content to help people Live After Success.